- Home

- Aircraft Financing

- Aviation Economics

- Search Articles

- Latest Issues

- Vol. 16 2026 >

- Vol. 15 2025 >

- January 9th 2025

- January 23rd 2025

- February 6th 2025

- February 20th 2025

- March 6th 2025

- March 20th 2025

- April 3rd 2025

- April 17th 2025

- May 1st 2025

- May 15th 2025

- May 29th 2025

- June 12th 2025

- June 26th 2025

- July 10th 2025

- July 24th 2025

- August 7th 2025

- August 21st 2025

- September 4th 2025

- September 18th 2025

- October 2nd 2025

- October 16th 2025

- October 30th 2025

- November 13th 2025

- November 27th 2025

- December 11th 2025

- Vol. 14 2024 >

- January 11th 2024

- January 25th 2024

- February 8th 2024

- February 22nd 2024

- March 7th 2024

- March 21st 2024

- April 4th 2024

- April 18th 2024

- May 2nd 2024

- May 16th 2024

- May 30th 2024

- June 13th 2024

- June 27th 2024

- July 11th 2024

- July 25th 2024

- August 8th 2024

- August 22nd 2024

- September 5th 2024

- September 19th 2024

- October 3rd 2024

- October 17th 2024

- October 31st 2024

- November 14th 2024

- November 28th 2024

- December 12th 2024

- Vol. 13 2023 >

- January 5th 2023

- January 19th 2023

- February 2nd 2023

- February 16th 2023

- March 2nd 2023

- March 16th 2023

- March 30th 2023

- April 16th 2023

- April 27th 2023

- May 11th 2023

- May 25th 2023

- June 8th 2023

- June 22nd 2023

- July 6th 2023

- July 20h 2023

- August 3rd 2023

- August 17th 2023

- August 31st 2023

- September 14th 2023

- September 28th 2023

- October 12th 2023

- October 26th 2023

- November 9th 2023

- November 23rd 2023

- December 7th 2023

- Vol. 12 2022 >

- January 6th 2022

- January 20th 2022

- February 3rd 2022

- February 17th 2022

- March 3rd 2022

- March 17th 2022

- March 31st 2022

- April 14th 2022

- April 28th 2022

- May 12th 2022

- May 26th 2022

- June 9th 2022

- June 23rd 2022

- July 7th 2022

- July 21st 2022

- August 4th 2022

- August 18th 2022

- September 1st 2022

- September 15th 2022

- September 29th 2022

- October 13th 2022

- October 27th 2022

- November 10th 2022

- November 24th 2022

- December 8th 2022

- Vol. 11 2021 >

- December 9th 2021

- November 25th 2021

- November 11th 2021

- October 28th 2021

- October 14th 2021

- September 30th 2021

- September 16th 2021

- September 2nd 2021

- August 19th 2021

- August 5th 2021

- July 22nd 2021

- July 8th 2021

- June 24th 2021

- June 10th 2021

- May 27th 2021

- May 13th 2021

- April 29th 2021

- April 15th 2021

- April 1st 2021

- March 18th 2021

- March 4th 2021

- February 18th 2021

- February 4th 2021

- January 21st 2021

- January 7th 2021

- Vol. 10 2020 >

- December 10th 2020

- November 26th 2020

- November 12th 2020

- October 29th 2020

- October 15th 2020

- October 1st 2020

- September 17th 2020

- September 3rd 2020

- August 20th 2020

- August 6th 2020

- July 23rd 2020

- July 9th 2020

- June 25th 2020

- June 11th 2020

- May 28th 2020

- May 14th 2020

- April 30th 2020

- April 16th 2020

- April 2nd 2020

- March 19th 2020

- March 5th 2020

- February 20th 2020

- February 6th 2020

- January 23rd 2020

- January 10th 2020

- Vol. 9 2019 >

- December 12th 2019

- November 28th 2019

- November 14th 2019

- October 31st 2019

- October 17th 2019

- October 3rd 2019

- September 19th 2019

- September 5th 2019

- August 22nd 2019

- August 8th 2019

- July 25th 2019

- July 11th 2019

- June 27th 2019

- June 13th 2019

- May 30th 2019

- May 16th 2019

- May 2nd 2019

- April 18th 2019

- April 4th 2019

- March 21st 2019

- March 7th 2019

- February 21st 2019

- February 7th 2019

- January 24th 2019

- January 10th 2019

- Vol. 8 2018 >

- December 13th 2018

- November 29th 2018

- November 15th 2018

- November 1st 2018

- October 18th 2018

- October 4th 2018

- September 20th 2018

- September 6th 2018

- August 23rd 2018

- August 9th 2018

- July 26th 2018

- July 12th 2018

- June 28th 2018

- June 14th 2018

- May 31st 2018

- May 17th 2018

- May 3rd 2018

- April 19th 2018

- April 5th 2018

- March 22nd 2018

- March 8th 2018

- February 22nd 2018

- February 8th 2018

- January 25th 2018

- January 11th 2018

- Vol. 7 2017 >

- December 14th 2017

- November 30th 2017

- November 16th 2017

- November 2nd 2017

- October 19th 2017

- October 5th 2017

- September 21st 2017

- September 7th 2017

- August 24th 2017

- August 10th 2017

- July 27th 2017

- July 13th 2017

- June 29th 2017

- June 15th 2017

- June 1st 2017

- May 18th 2017

- May 4th 2017

- April 20th 2017

- April 6th 2017

- March 23rd 2017

- March 9th 2017

- February 23rd 2017

- February 9th 2017

- January 26th 2017

- January 12th 2017

- Vol. 6 2016 >

- December 15th 2016

- December 1st 2016

- November 17th 2016

- November 3rd 2016

- October 20th 2016

- October 6th 2016

- September 22nd 2016

- September 8th 2016

- August 25th 2016

- August 11th 2016

- July 28th 2016

- July 14th 2016

- June 30th 2016

- June 16th 2016

- June 2nd 2016

- May 19th 2016

- May 5th 2016

- April 21st 2016

- April 7th 2016

- March 24th 2016

- March 10th 2016

- February 25th 2016

- February 11th 2016

- January 28th 2016

- January 14th 2016

- Vol. 5 2015 >

- December 17th 2015

- December 3rd 2015

- November 19th 2015

- November 5th 2015

- October 22nd 2015

- October 8th 2015

- September 24th 2015

- September 10th 2015

- August 27th 2015

- August 13th 2015

- July 30th 2015

- July 16th 2015

- July 2nd 2015

- June 18th 2015

- June 4th 2015

- May 21st 2015

- May 7th 2015

- April 23rd 2015

- April 9th 2015

- March 26th 2015

- March 12th 2015

- February 26th 2015

- February 12th 2015

- January 29th 2015

- January 15th 2015

- Vol. 4 2014 >

- December 18th 2014

- December 4th 2014

- November 20th 2014

- November 6th 2014

- October 23rd 2014

- October 9th 2014

- September 25th 2014

- September 11th 2014

- August 28th 2014

- August 14th 2014

- July 31st 2014

- July 17th 2014

- June 19th 2014

- July 3rd 2014

- June 5th 2014

- May 22nd 2014

- May 8th 2014

- April 24th 2014

- April 10th 2014

- March 27th 2014

- March 13th 2014

- February 27th 2014

- January 30th 2014

- February 13th 2014

- January 16th 2014

- January 2nd 2014

- Vol. 3 2013 >

- December 5th 2013

- November 21st 2013

- November 7th 2013

- October 24th 2013

- October 10th 2013

- September 26th 2013

- September 12th 2013

- August 29th 2013

- August 15th 2013

- August 1st 2013

- July 18th 2013

- July 4th 2013

- June 20th 2013

- June 6th 2013

- May 23rd 2013

- May 9th 2013

- April 25th 2013

- April 11th 2013

- March 28th 2013

- March 14th 2013

- February 28th 2013

- February 14th 2013

- January 31st 2013

- January 17th 2013

- January 3rd 2013

- Vol. 2 2012 >

- December 6th 2012

- November 22nd 2012

- November 8th 2012

- October 25th 2012

- October 11th 2012

- September 27th 2012

- September 13th 2012

- August 30th 2012

- August 16th 2012

- August 2nd 2012

- July 19th 2012

- July 5th 2012

- June 21st 2012

- June 7th 2012

- May 24th 2012

- May 10th 2012

- April 26 2012

- April 12 2012

- March 29 2012

- March 15 2012

- March 1 2012

- February 16 2012

- February 2 2012

- January 19 2012

- January 5 2012

- Vol. 1 2011 >

- Jurisdictions

- Supported Content

- Subscribe/Login

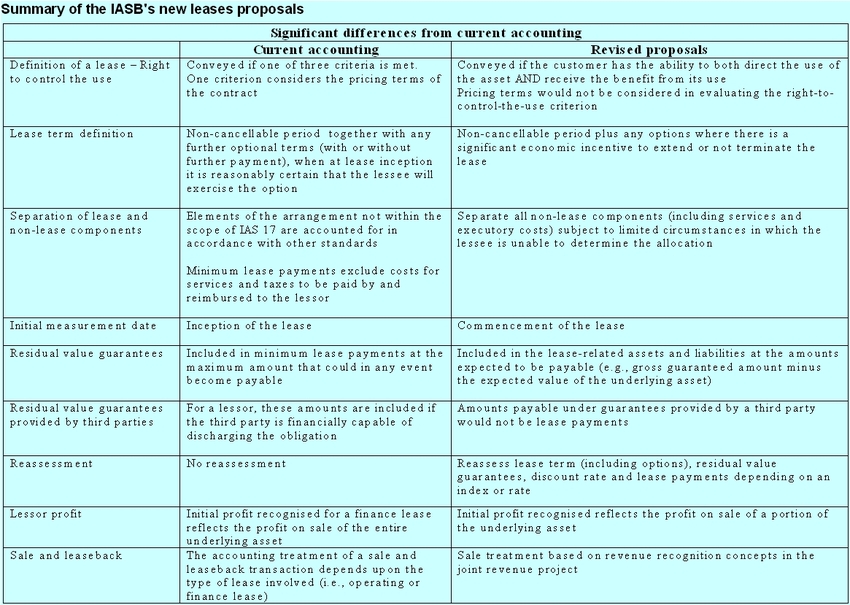

The 'all-you-need-to-know' guide for lessors on the state of play of the IASB and FASB proposals on leases

The 'all-you-need-to-know' guide for lessors on the state of play of the IASB and FASB proposals on leases Revised lease accounting proposals 'a compromise too far'

Revised lease accounting proposals 'a compromise too far' 'With three generations of planes out there, anyone buying classics has a potential greater residual risk'

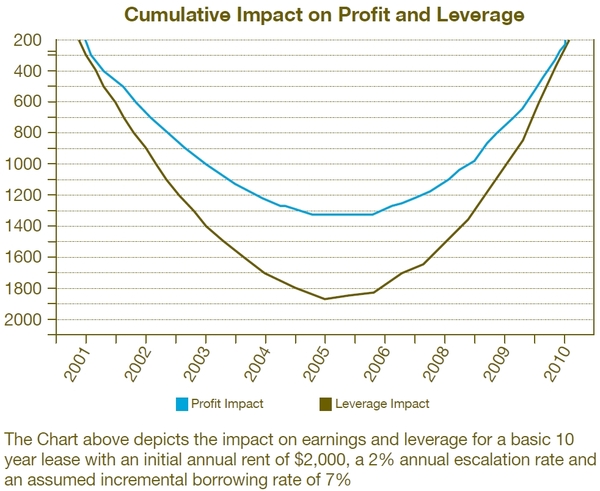

'With three generations of planes out there, anyone buying classics has a potential greater residual risk' Overhaul of Lease Accounting to bring fundamental changes to reported Performance and Leverage

Overhaul of Lease Accounting to bring fundamental changes to reported Performance and Leverage Top auditors on capital issues and new standards

Top auditors on capital issues and new standards Interview: IASB-FASB on lease accounting, as new standard begins to take final shape

Interview: IASB-FASB on lease accounting, as new standard begins to take final shape The benefits of using Cayman Islands and Irish vehicles in aircraft finance transactions

The benefits of using Cayman Islands and Irish vehicles in aircraft finance transactions Boards to re-expose leases - a new approach for lessors selected

Boards to re-expose leases - a new approach for lessors selected- © 2026 Fintel Ltd

- Privacy

- About Us

- Contact Us