- Latest edition July 9th: 10 billion annual air passengers by 2045

- June 25th: Mid-life aircraft opportunity

- June 11th: Airline profits to slide

- May 28th: Retirement rates and increased deliveries

- May 14th: Spirit complications

- April 30th: Demand for aviation assets solid despite airline industry challenges

|

Boards to re-expose leases - a new approach for lessors selected

The FASB and the IASB are inviting comments on their latest proposals for joint leases, as questions remain about the receivable and residual approach writes Ernst & Young's John McCormack.

The Financial Accounting Standards Board (FASB) and the International Accounting Standards Board (IASB) - collectively known as the Boards - have confirmed that they will, for a second time, offer constituents a chance to comment on proposed changes to their joint leases proposal having made significant changes to the model originally proposed last year.

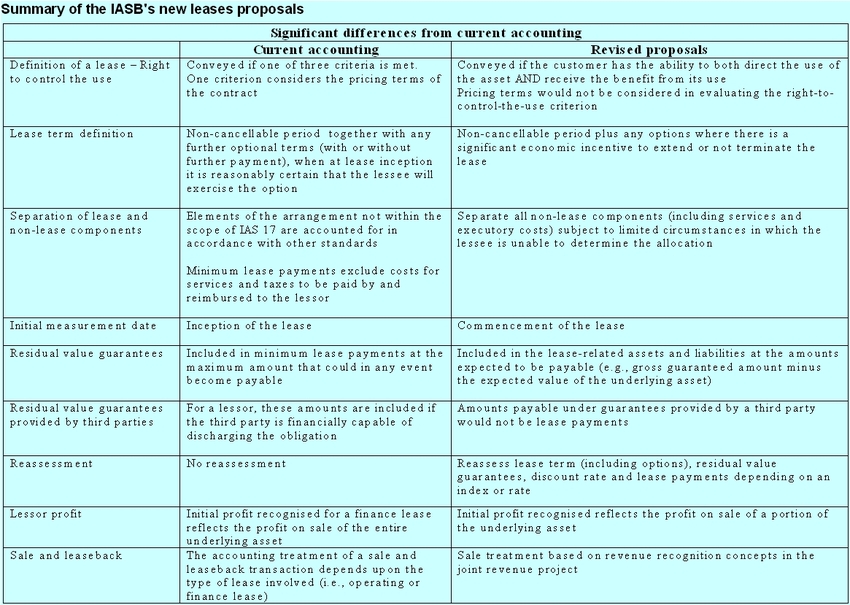

In short: - They are developing a new approach to lessor accounting that is significantly different to current accounting and the proposals in last year’s exposure draft. - Their proposed accounting would be significantly more complex than the current lessor model. - Under the new approach all lessors should apply a single approach, the Receivable and Residual approach, to all leases, subject to the exceptions noted below. - Under their new proposals, lease receivables would be recognised for all leases (subject to the exceptions noted below), a portion of the carrying amount of the underlying leased asset would be re-characterised as a residual asset and the remainder would be derecognised. - Under their new proposals, the timing and pattern of lessor profit recognition would depend on whether the profit in the lease is ‘reasonably assured’. The Boards decided that lessors should apply a single approach to all leases, with a few exceptions. This represents a significant change from current lease accounting and the proposals in last year’s exposure draft (ED). Other significant lessor changes are detailed in Appendix I below. The Boards still need to discuss other lessor-specific issues, including the interaction with the financial instruments project, changes in lease agreements, residual value guarantees, impairment, financial statement presentation, disclosure and transition. All of the decisions made by the Boards to date are tentative and will not be finalised until the Boards approve a final standard. Seeking feedback on the changes proposed to the leases will give constituents a chance to express their views on the changes proposed. Lessor accounting Under the model proposed in the last year’s ED, lessors would apply one of two approaches based on whether the lessor retains exposure to significant risks or benefits associated with the underlying asset. Feedback on the ED’s original lessor accounting model was mixed. Some favoured having one approach only. Others questioned whether the proposal represented an improvement over existing guidance for lessors and encouraged the Boards to retain the current model. The Boards recently agreed that lessors should apply a single approach, the Receivable and Residual approach, to all leases, subject to the following two exceptions: - Investment properties - Investment property entity lessors would not apply the lessor model to leases of investment properties - Short-term leases - Lessors could make an accounting policy election to apply current operating lease accounting to short-term leases. A short-term lease would have a maximum possible lease term, including any options to renew, of 12 months - The Boards previously made decisions on other key lease concepts, including definition of a lease, lease term, lease payments and discount rate. The Boards decided that lessors would be required to separate all non-lease components (including services and executory costs) and lease components using the allocation method proposed in the joint revenue recognition project (i.e., on a relative selling price basis in most cases). Receivable and Residual approach Under the Receivable and Residual approach, upon commencement of the lease, the lessor would: - Recognise a lease receivable for the lessor’s right to receive lease payments - Allocate the carrying value of the underlying asset being leased between the portion related to the right of use granted to the lessee and the portion retained by the lessor (i.e., the residual asset) - Recognise profit, if profit is reasonably assured, or any indicated loss The lease receivable would be initially measured at the present value of the lease payments over the lease term discounted using the rate the lessor charges the lessee. lessors would determine the lease term and lease payments using the same principles applied by lessees (e.g., exclude usage-based contingent rents). The allocation of the carrying amount of the underlying asset would be based on the ratio of the initially measured lease receivable to the fair value of the underlying asset being leased. If the profit under the lease is reasonably assured, the residual asset recognised is initially measured as:

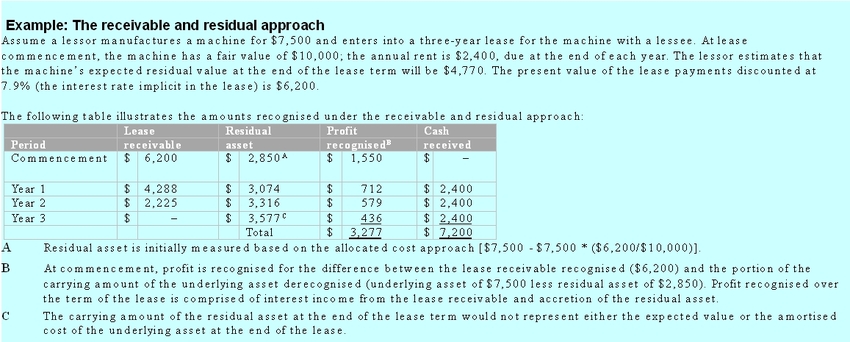

The portion of the carrying amount of the underlying asset allocated to the right of use granted to the lessee would be derecognised. At the commencement of the lease, profit or loss would be recognised for the difference between the lease receivable recognised and the portion of the carrying amount of the underlying asset derecognised. This is as opposed to the current finance lease accounting, where the initial profit recognised reflects the profit on the sale of the entire asset and not just the portion leased. The receivable and residual approach would result in lower initial profits being recognised for this type of lease. Over the term of the lease, the Lessor would recognise interest income from the right to receive payments and accrete the residual asset. Both the interest income and accretion income would be calculated using the rate the lessor charges the lessee. A detailed worked example is attached at Appendix II. In addition, the lessor would recognise profit upon commencement only when that profit is reasonably assured. The reasonably assured threshold is intended to align the recognition of profit by lessors with principles developed by the Boards in their joint revenue recognition project. The Boards discussed instances in which profit may not be reasonably assured, such as when the residual value at the end of the lease term or the day one fair value cannot be estimated. They indicated that Lessors would rely on experience or other persuasive evidence, assuming that experience is predictive of the outcome of the lease contract in question, for such estimates. If the profit is not reasonably assured, no profit would be recognised at lease commencement and the residual asset would initially be measured as the difference between the lease receivable and the carrying value of the underlying asset. The residual asset would be accreted over the lease term to an ending amount equivalent to the underlying asset’s carrying amount at the end of the lease term as if it had been subject to depreciation using its original depreciable life and salvage value. That is, the lessor would recognise income using a constant rate of return over the lease term to accrete the residual asset to the amount that the underlying asset would have been measured at if it had remained on the balance sheet of the lessor and been subject to depreciation. Interest income on the lease receivable would be recognised over the lease term using the interest rate the lessor charges the lessee. The Boards' decision is intended to encourage commentary as Lessors evaluate the impact of the proposed revised model. Certainly, questions remain about how to apply the Receivable and Residual approach to lessor accounting and additional guidance and clarification is expected on this over the coming months as the Boards prepare an updated proposal for re-exposure.

John McCormack is Ernst & Young Ireland's Aviation Sector Leader This article was first published in Aviation Finance, in September 15th 2011 |