- Latest edition August 6th: ACG aims to become a Top 5 lessor

- July 23rd edition: Aviation ABS issuance has already surpassed the prior full-year record for 2025.

- July 9th: 10 billion annual air passengers by 2045

- June 25th: Mid-life aircraft opportunity

- June 11th: Airline profits to slide

- May 28th: Retirement rates and increased deliveries

|

P2F conversion market is gaining momentum

The potential afforded by the passenger-to-freight (P2F) conversion market to aviation sector investors was highlighted recently in a webinar by IBA's Moshe Haimovich (right) and Phil Seymour. It comes against the backdrop of a surge in freight volumes in the first half of 2017 as reported by IATA. Significant expansion of the freighter fleet is expected over the next 20 years, virtually all of it deriving from P2F conversion.

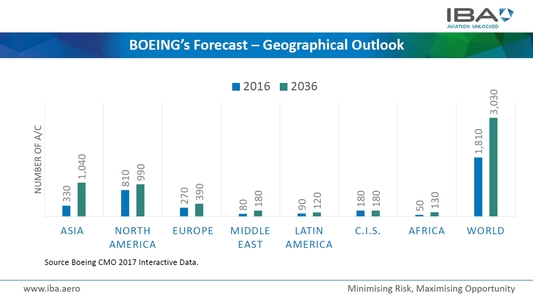

Airbus, for example, forecasts that the global freighter fleet will grow from an estimated 1,610 last year by a net 800 to 2,410 over the next 20 years. Boeing puts the likely growth at 1,220 new aircraft to 3,030 aircraft over the same period. These figures comprise new factory freighters and conversions, offset by retirements over the period.

Boeing's projections for the period include 460 widebody conversions and 1,100 narrowbody, with 920 new freighter deliveries all being widebodies. The manufacturer sees the biggest growth potential far by far as being in Asia, where it expects the freighter fleet to more than treble from 330 in 2016 to 1,040 in 2036.

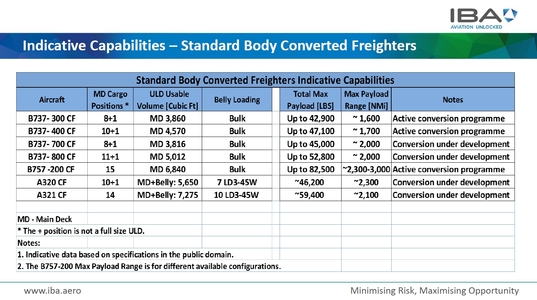

The webinar was co-presented by IBA CEO Phil Seymour and freight aircraft industry veteran Moshe Haimovich,who recently joined IBA to head up a new freighter advisory practice within the firm. The discrepancies between the two manufacturers figures, Haimovich pointed out in the webinar, was due to differences in exactly what aircraft they include. This is not an exact 'apple to apple comparison,' he said, but it still provided a clear indication of the expected future trend. IBA identified P2F conversion programmes currently available for five aircraft types, with conversion costs ranging from $2.3 million for AEI's MD80 up to between $13-15 million for Boeing and AIA's B767-300ER programmes. However, IBA also identified programmes under development for a further five aircraft families, including the B737-700 and 800, A320/A321, A330-200 and -300, and possible programmes for the B777-200ER and -300ER which are under consideration by Boeing and IAI. As well as looking at a B737-800 case study to explore the underlying economic principles and issues of a typical mid-life narrowbody conversion, the IBA experts gave their views on differences in the types of aircraft most suitable conversion and some of the many factors influencing investor decisions in the conversion space. Seymour noted that from 12 years on, coinciding with the end of the typical first lease period, there is a focus on whether to extend the lease, part-out or convert to freighter. The market is still enjoying low fuel prices and increased demand from freighter and packaging businesses, he said. This coincides with increased availability of suitable feedstock as the next generation aircraft arrive, particularly in terms of the B737 and A320 families as well as the A330 and B777s.

Haimovich said that while the industry could expect to see further conversions of B757-200s, the A321 would definitely be its successor because of its loading options, with 14 cargo positions on the main deck and further capacity on the lower deck giving the equivalent to 17 main deck positions. 'The trend in the market is for upsizing, so the big question that is asked in the market is are operators going straightforward on the B737-800 or is it going to be gradually from 700 and then 800?' he said. The same was true the A320 and A321. 'Taking account of the large feedstock availability on the two larger aircraft, in our opinion the market will go the upsizing,' he continued. 'We can see already now there are about 200 order/options backlog on the 737-800 and the A321 will be the first freighter conversion developed by EFW.' Furthermore, as the age of aircraft and their values have dropped sufficiently on the A320 family and the 737NGs, that seemed to make this an economically viable situation, he added. Haimovich noted that the average age of the existing 737-300 and -400 freighter fleet is now high. The average age of the 400 fleet is almost 24 years and the -300 fleet is 26 years. With limited availability of suitable -300 feedstock now and a similar position for the -400, with some continued availability for the next two to three years, to meet future demand the market will need to switch to new generation feedstock, he said. And in terms of value from the investment, the 737-800 would be more capable than the -400 and the A321 would be the natural successor to the 757-200. Moving forward, Seymour said, from 2020/21 we are going to see more conversions of new generation aircraft. In terms of widebody conversions, there would be a reduction in the availability of suitable P&W powered feedstock for the B767-300ER and strong interest in the A330-300 conversion progamme currently under development, offering more positions both on the main deck and in the belly of the aircraft, something reflected in DHL's recent order for eight of them. Seymour emphasised that P2F conversion should not be regarded as a speculative investment. 'You need to have all your ducks in a row,' he said. 'There's a lot of analysis and maintenance planning needed to ensure selection of the right aircraft.' The full IBA webinar can be viewed here. |

Vol. 7 Issue 19 of Aviation Finance