|

First $1 billion+ aircraft ABS since 2008

The demand from investors for aviation assets, and the strong return of the aircraft-backed ABS market is evident as the first $1 billion+ aircraft ABS is readied for market. The issuance, structured by Canada's Element Financial Corporation, will be backed by 49 narrowbody and widebody aircraft. The $1.2 billion ABS shows the strength of investor demand for aviation assets and the opportunity that exists for aircraft lessors to issue ABS. The demand for aircraft assets from investors is seeing a slew of aircraft-backed ABS' being lined up with the Element transaction expected to be followed by issuances from BOC Aviation, SMBC, AWAS and GECAS.

A $1.2 billion ABS backed by 49 aircraft, and structured by Element Financial Corporation, shows the strength of investor demand for aviation assets and the opportunity that exists for aircraft lessors to issue ABS. The demand for aircraft assets from investors is seeing a slew of aircraft-backed ABS' being lined up with the Element transaction expected to be followed by issuances from BOC Aviation, SMBC, AWAS and GECAS. The Element-structured transaction, ECAF I, will be backed by 49 commercial aircraft across three tranches of notes for a total amount just in excess of $1.2 billion, and will the first aircraft ABS issuance since 2008 to break the $1 billion barrier.

The issue has a number of innovative features that are commented upon favourably by the rating agencies; including the following: - The transaction has performance triggers, including aircraft utilization (75% for cash sweep) and DSC ratios (1.15x for cash sweep), to speed up principal amortization if the trigger tests fail; - It has a maintenance reserve top-up mechanism based on a third-party appraiser's maintenance cash flow forecast, and, - It has a liquidity facility that will cover nine months of scheduled interest (excluding step-up amount) on the class A-1, A-2, and B-1 notes at closing. BBAM through its Irish subsidiary, BBAM Aviation Services Limited, will be servicer of the assets and the proceeds from the sale of the notes will finance the acquisition of 49 aircraft from entities managed by affiliates of BBAM. BBAM has a managed fleet of over 400 aircraft, including those of listed lessor FLY Leasing. Both Fitch and S&P have issued presale reports on the issuance with the A tranches - $459.375 million A-1 notes and $590.625 million A-2 notes - rated A by both agencies. The B-tranche $160 million B-1 notes has been rated BBB by both. All three tranches have maturity dates of May 2040.

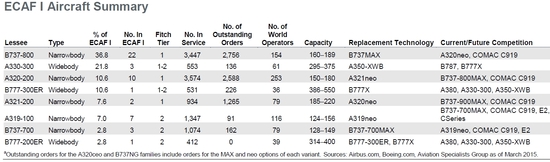

The 49 aircraft are on lease to 38 lessees with the average age of the aircraft at 6.5 years, with 5.9 years on average remaining on the leases. By value 64.9 per cent of the portfolio are narrowbody with remainder widebody. The portfolio is made up of Boeing (52.9%) and Airbus (47.1%) aircraft. The largest lessee is Singapore Airlines (14.6%), with Philippines Airlines (11%), LATAM (10.6%), Aeroflot (6.7%) and Pegasus (5.5%) rounding out the top five. The top three concentrations by country are Singapore (16.1%), Philippines (11%) and Chile (10.6%). 66.5% of the pool is concentrated with airlines such as Etihad, which are designated as flag carriers for their respective countries. Canadian equipment finance group Element Financial Corporation is acting as structuring agent and administrator on the issuance with BNP Paribas acting as liquidity facility provider, and Deutsche Bank Securities, BNP Paribas and Citigroup Global Markets acting as joint lead bookrunners. In a note on the technological risk attaching to the various aircraft models contained in the poetfolio, Fitch said that "all aircraft in the portfolio are expected to be exposed to increasing competitive pressure over the course of the transaction from existing manufacturers and new entrants to the market". It outlined its specific thinking, by class of model as follows: "neo” and “MAX”: Airbus and Boeing have introduced replacement programs for the A320ceo and 737NG families with the “neo” and “MAX” programs. Initial deliveries of the “neo” and “MAX” aircraft are anticipated in 2015 and 2017, respectively. Twin-engine Widebodies: Airbus recently launched the twin-engine widebody A350XWB, delivering its first plane to Qatar Airlines in December 2014, and views the plane to be a replacement for the A330-300. Boeing is also in the production process for a new twin-engine widebody plane with its B777X, but the program is not expected to hit the market until 2019. Both of these new variants are expected to affect the demand profile of the A330-300s and B777-300ERs in the future. E Series: Embraer plans to revamp its regional jets with new-technology engines and introduce the E2 family in 2018 to the market. These jets are expected to create pressure on not only the current E190 fleet, but also the shorter variants within the A320ceo and 737NG families. C Series: The C-Series aircraft, which Bombardier projects will burn 20% less fuel than competitors, is expected to enter service in 2016 after numerous delays in the production process. The aircraft is expected to compete directly with the shorter variants in the A320ceo and 737NG families, in addition to Embraer’s regional jets. COMAC: Commercial Aircraft Corporation of China’s (COMAC) long-planned C919 is slated to enter service in 2018 and compete directly with the A320ceo and 737NG families. "While Fitch does expect deterioration in values and lease rates to result, the long lead time it will take to replace the current-generation aircraft will insulate the aircraft in the near to medium term", it says in its presale. The legal structure of ECAF1 ECAF I is a newly established, bankruptcy-remote, special-purpose, exempted company incorporated under the laws of the Cayman Islands and is a resident of Ireland for tax purposes. Aircraft may be owned by individual, newly established SPEs (lessors) that are 100% owned by ECAF I (subject to any agreed local requirement or other exceptions). A charitable trust formed under the laws of the Cayman Islands will own 100% of the common shares of ECAF I. ECAF I will have a board consisting of 3 directors with at least 1 director independent from the servicer, administrator, issuer and any affiliate thereof. Fitch in its presale says that it believes the legal structure of the transaction provides that a bankruptcy of BBAM, EFC or affiliated entities as sellers "would not impair the timeliness of payments on the notes...Fitch has received and reviewed legal opinions to the effect that the transfers of the leases, aircraft and beneficial interests in the SPEs to ECAF I and its subsidiaries constitute a true sale and not a secured financing, and the assets of ECAF I would not be consolidated with those of BBAM, EFC or affiliated entities in the event of bankruptcy. Furthermore, Fitch has received an opinion of counsel that the trustee would have a first-perfected security interest in the assets transferred to ECAF I". Scheduled Amortization of the Notes Class A: (A1: $459.38m. ;A-2: $590.63m.; B1:$160.0m. (Total: $1,210m) Class A: Scheduled straight-line amortization to zero over 16 years. Only the A-1 notes will receive scheduled principal for the first seven years, based on a scheduled straight-line amortization to zero over those seven years. The entire balance of class A-2 notes will be due and payable on the expected maturity date, with no amortization over the first seven years. Class B: Scheduled straight-line amortization to zero over 16 years. The outstanding balance of class B1 notes will be due and payable at the expected maturity date. Note: Following the sale of aircraft, the amortization schedule shall be adjusted to maintain the straight-line amortization profile. In addition, there will be a cash sweep or trap amortization of ECAF I’s distributions based on performance covenants, including the debt service coverage ratio (DSCR) and utilization tests. S&P in an overview of the aircraft leasing sector business outlook says in its presale: "According to Airbus and Boeing forecasts, airline passenger traffic is expected to grow by 5%-6% per year through 2031 with most of the growth coming from the Middle East and Asia-Pacific regions. Airbus is forecasting 26,350 new passenger aircraft deliveries, and Boeing forecasts 34,000 during that period. Most of the aircraft will either be delivered to Asia-Pacific and emerging markets to meet demand or to replace aging aircraft in North America and Europe. "The number of lessor-owned aircraft has been steadily growing. Operating leases currently account for around 40% of the global commercial fleet and could grow to around 50% in the next five to 10 years. Aircraft leasing is attractive to airlines because of lower capital outlay requirements, fleet planning flexibility, delivery position availability, and residual value risk avoidance. On Jan. 1, 2013, export credit financing costs increased for aircraft because higher pricing and equity contributions, which resulted in more airlines finding it more cost efficient to lease aircraft. We expect lessors to continue to assume some airline orders for new aircraft through sale/leaseback transactions because of this development. In addition, the lessors generally are more creditworthy, which gives them better access to capital at more attractive pricing than many airlines. "The recent European sovereign debt crisis has forced some banks to reduce their involvement in traditional aircraft bank lending, which had been a major source of funding for the aircraft lessors and the aviation industry. As a result since 2011 many aircraft lessors have turned to the capital markets to raise secured and unsecured debt to fund new aircraft deliveries and refinance debt maturities. More recently, many European banks have increased their lending to the sector. Banks in other regions, particularly in Asia, have also either increased their lending or entered this space for the first time, and some aircraft lessors have obtained equity investments. For example, early in 2013, Onex Corp. invested in FLY Leasing Ltd. (FLY) and its affiliate, BBAM, and in July 2013, Fly received proceeds of $184 million from a secondary offering. Marubeni Corp. also invested $209 million in Aircastle Ltd. in July 2013. In May 2014, AerCap Holdings N.V. acquired competitor International Lease Finance Corp. (ILFC). The combined organization is the second-largest aircraft lessor behind GE Capital Aviation Services in terms of the number of aircraft. (ILFC was he second-largest before the acquisition.) In December 2014, Avolon Holdings Ltd. completed an IPO." S&P's on the transactions weaknesses: The transaction's weaknesses are: - Cyclical demand, aircraft lease rates, and customer airlines' frequent weak credit quality are inherent risks in the aircraft leasing business. Although lease rates for certain aircraft types have been under pressure in the past few years, recent evidence suggests that lease rates have stabilized or have even begun to improve. In addition, economic weakness in the eurozone (European Economic and Monetary Fund), which resulted in many airline bankruptcies and aircraft repossessions for aircraft lessors earlier in the decade, has abated though not fully recovered. Also, access to capital, which was a concern when European banks reduced lending to the aviation sector in 2011, has actually continued to be available with many banks worldwide (including in Europe) and capital markets transactions accounting for larger shares of industry financing. - Although this fleet comprises generally popular aircraft, the weighted average aircraft age (6.7 years) is a little older than that of the recent aircraft ABS transactions, which ranges from two years to 6.1 years. - The class A-2 notes' amortization schedule is slower than other aircraft-backed transactions we rated 'A (sf)'. - Many of the lessees have low credit quality, which is typical for aircraft lease securitizations. - All of the aircraft are expected to be transferred to the issuer after the transaction closes and before the delivery expiration date (270 days after closing). If an aircraft is delivered into the transaction between the closing date and the delivery expiration date, the seller will receive the rents associated with this aircraft during the period between the closing date and the aircraft delivery date, and these rents will not be transferred into the transaction. These rents will be credited against the purchase price of such aircraft when the aircraft is delivered into the transaction. Therefore, there is negative carry on the note interest, and there may be no principal amortization or not enough cash to cover the scheduled principal payment amount of the issuer's notes before the aircraft delivery date. (All the aircraft will cross-collateralize all of the notes, and so to the extent there is cash available to amortize the notes from rents received from any aircraft that have been funded, that cash will be used to pay amortization on the notes.) S&P on the factors that mitigate the weaknesses: The following factors partially mitigate the transaction's weaknesses: - Our cash flow assumptions, which consider the initial and future lessees' credit quality, as well as the lessee and aircraft model concentrations. - Our lease rate model, which is periodically calibrated to reflect up-to-date lease yield levels. Lease rate factors are lower today than in recent years. - The presence of some stronger lessees in the portfolio, though many of the lessees have low credit quality. - Our projected default rates, which the default simulator (a Monte Carlo simulation model [Standard & Poor's Collateralized Debt Obligation (CDO) Evaluator]) generates, considered the lessee concentration, industry correlations, and country correlations. - The incorporation of additional sensitivity analyses focused on end-of-useful-life assumptions (with shorter lives for the selected models) and lease rates in addition to our June 2010 published standard cash flow stress assumptions. - The favorable aircraft type in the portfolio, which somewhat compensates for the aircraft type concentration. - The E note purchase account will cover the negative carry on the note interest before aircraft delivery. The E note purchase account, initially funded in the amount of the E note issuance amount minus closing fees and the initial maintenance reserve, will cover both the interest and senior expenses shortfall (prior to liquidity drawing) before the delivery expiration date. On the aircraft delivery date, the class E aircraft allocation amount will be paid from the E note purchase account to the seller. On the delivery expiration date, the balance on the E note purchase account will be transferred to the transaction's collection account to follow the applicable priority of payment. This article first appeared in: Vol. 5 Issue 10 of Aviation Finance, (May 21 2015) May 21st 2015. |

Vol. 5 Issue 10 of Aviation Finance