- Latest edition April 30th: Demand for aviation assets solid despite airline industry challenges

- April 16th: Sumisho ALC gets off the ground

- April 2nd: Jet fuel prices and airline hedging strategies

- March 19th: Air travel to more than double by 2050

- March 5th: DAE to acquire Macquarie AirFinance

- February 19th: Lessors report record 2025 performance

|

Airports and Airlines: the gains to be made by a more productive working relationship

JOHN CARTER, managing director of AviaSolutions, GECAS' independent consultancy division, looks at a key aspect of how the growth of low cost carriers (LCCs) has brought new competition to the airport sector. With LCCs having the common desire to minimize operating costs and full-service carriers placing different demands on an airport’s capital infrastructure, the objectives of airlines and airports may not always be perfectly aligned. Carter says that working with both airlines and airports on a regular basis, AviaSolutions have seen at first-hand how operations can be improved at every level of both businesses to create mutually beneficial scenarios for both parties. He says there is a trend for the adversarial airline/airport relationships of the past to begin to become one based on partnership.

Ask any airline CEO who his customer is and his answer will be clear: “the passenger.”

Ask any airport CEO who his customer is and the answer is generally more ambiguous: “it’s the passenger,” or “it’s the airline,” or both.

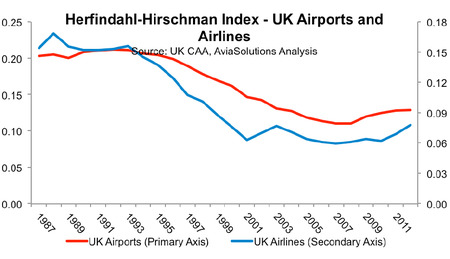

This lack of distinct focus on one customer type has led to a wide range of airport business models across the world. Add the wide variety of airline business models - from ultra-low cost carrier (LCC) to full-service airline to regional feeder airline - and it’s easy to see how the objectives of airlines and airports may not always be perfectly aligned. - Full-service carriers place different demands on an airport’s capital infrastructure than LCCs, forcing airport operators to have varied, often unfocused but adaptable business models. - LCCs have in common a desire to minimize operating costs, but perversely, supporting this objective may require additional airport investment to develop secondary “low operating-cost” facilities. The relatively recent and rapid growth of LCCs around the world has had a profound impact on airport economics, and at AviaSolutions we are observing a number of trends that will impact the three main stakeholders: passengers, airports and airlines. Our extensive track record of delivering practical advice and detailed financial modeling expertise to airports, airlines, investors and lenders alike, gives us an insider view on the airline and airport perspectives. The growth of the LCC airlines has brought significant new competition to the airport sector. Often large city airports are eschewed in favor of out-of-town secondary airports to secure lower operating costs. In doing so, LCCs have been able to bring new passengers to the market through the introduction of significantly lower fares. This trend has contributed to a reduction in average airport charges per passenger (aeronautical yield), though undoubtedly also driving higher traffic volume and total airport revenue (aeronautical and non-aeronautical). A quick look at the Herfindahl-Hirschman Index (HHI)* in the UK airport and airline sectors indicates that market concentration has declined for both of these stakeholders over the recent years as a result of this increased competition. British Airways flights from London Heathrow to most European destinations are now subject to intense competition from other London airports, which was evidently not the case 15-20 years ago. Interestingly, the recent economic downturn since 2008 has seen a reversal of this trend as LCCs have consolidated services into the larger airports. At the same time, the scale of airport privatization has increased, with shareholder interests driving a more commercially focused approach to airport operations. Over the last decade, airport management has increasingly shifted its focus to maximizing non-aeronautical revenue from the passenger to help meet its more aggressive business targets, and offset the downward pressure on aeronautical charges. The airlines, led by the LCCs, are doing the same, seeking to offset low fares (RASK) with additional revenues from ancillary activities. The increasingly competitive market and profitability challenge highlights the need for airports and airlines to cooperate in order to ensure a higher quality and more sustainable experience for the passenger. Working with both airlines and airports on a regular basis, we at AviaSolutions have seen first-hand how operations can be improved at every level of both businesses to create mutually beneficial scenarios for both parties. We understand the growing importance for airports and airlines working together.

One of the key challenges is to get airports and airlines to better understand the symbiotic nature of the economic relationship. - Does an airport understand how airline fuel costs and turn times impact profitability? - Do airlines understand the reasoning behind the proportion of airport charges attributable to passengers versus movements? - Do airlines understand the significance of single versus dual till economic regulation? We believe there is a trend for the adversarial airline / airport relationships of the past to begin to become one based on partnership. New financial arrangements require stronger business models, more detailed data analysis and global experience in the aviation sector. These changes have started to bring some airport and airlines closer together. It is early days, and making airline and airport business models align is easier said than done. But we see the more forward-thinking management teams adapt their long-standing ambivalence towards each other. For example: - In Dubai, the airport just opened a new T3 satellite designed with 22 gates specifically for Emirates’ fleet of Airbus A380s. - At London Heathrow, British Airways worked very closely with the airport to develop T5. - At Kuala Lumpur, KLIA built a low-cost terminal facility for Air Asia. - Copenhagen Airport opened a low-cost facility that will allow all airline models to work effectively under one roof. With the digital age truly upon us and airports and airlines sharing the same customer (“the passenger”) a world of opportunity is opening for those parties that are able to work together and provide an appropriate customer experience, and seamlessly manage the entire travel process from booking to arrival at the destination. Data sharing is becoming an increasingly important component of this development and will continue to be so. AviaSolutions is acutely aware of these developing trends and is supporting clients seeking to tackle these complex issues. One area we are exploring is how the interrelationship between airlines and airports will affect airline fleet planning decisions. Passengers will surely benefit as more airlines and airports work together more efficiently and productively. It is our view that that airlines and airports will also benefit. * The Herfindahl-Hirschman Index (HHI) is an economics measure of market concentration, based on the market shares of the participants in a particular market. (It is the sum of squares of the market shares, expressed as a fraction, of the top 50, or less, firms in the sector). John Carter is managing director of AviaSolutions the independent consultancy division of GE Capital Aviation Services (GECAS). August 1st 2013. |

Vol. 3 Issue 16 of Aviation Finance