|

Leasing can provide an attractive investment opportunity for long-term equity investors: Forsberg.

The aviation leasing sector can provide an attractive investment opportunity for long-term equity investors looking to achieve steady risk-adjusted equity returns while participating in the growing global aviation business writes Avolon's DICK FORSBERG.

Investing in aircraft leasing equity provides a number of attractive features, including:

- Compelling economics and track record of resilient profitability; - A long-term investment horizon; and - Attractive equity returns through the cycle, enhanced by active portfolio management

Within the aviation value chain, lessors provide a more profitable and less risky vehicle for investment in the aviation industry than investing directly in the airlines. Aircraft lessor equity returns are a function of purchase price, sale price, lease income stream, overhead expenses and the cost of financing. The strong value retention and liquidity of aircraft, especially younger models, support high levels of leverage, historically as much as 80% of an aircraft’s Market Value, which, along with cost of borrowing, is a key driver of enhanced equity returns. A skilled aircraft lessor management team experienced in sourcing and divesting assets at attractive valuations, managing the residual value risk of its portfolio, marketing aircraft to a range of airlines to maximize lease income and arranging low-cost debt facilities can generate substantial equity returns for investors in aircraft.

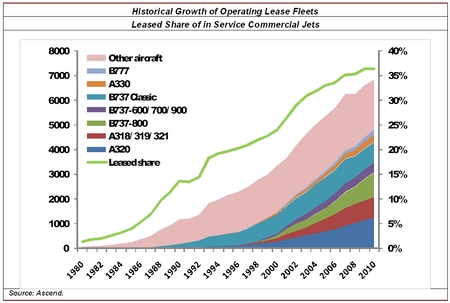

Commercial aircraft leasing is a global business with attractive growth dynamics. The role of aircraft lessors has expanded significantly over the past 30 years as airline fleets have grown and fixed costs for maintenance and ownership of assets increased. As a result, airlines have increasingly turned to aircraft lessors to finance their fleet growth and replacement requirements and lessors have become a constant source of financing for this global aviation business sector. The continued growth in the number of aircraft on operating leases is fundamentally the result of three principal drivers. The first is that the use of operating leases enables airlines that do not have ready access to capital, or that find the cost of debt financing too burdensome, to acquire new or relatively new aircraft that otherwise would be prohibitively expensive. Secondly, it provides airlines with a degree of fleet flexibility that would not be possible with owned or debt-financed aircraft. Thirdly, it is an important element of diversified fleet financing strategies, even for airlines that are able to raise finance in the commercial markets. In 1990, there were 1,200 aircraft on operating lease, representing 14% of the commercial jet fleet. By 2000 the number of aircraft on lease had risen to 3,400, accounting for 24% of the total and by 2010 the market had reached 6,800 leased jets, representing over 36% of all commercial jets. The majority of these include popular A320 and 737 family members, a growing number of 777s and A330s and a significant number of older, mostly out of production, equipment. The leased aircraft share of the global fleet is expected to increase further as global passenger traffic and commercial jet fleets maintain strong underlying growth trends, forecast at CAGRs of 5.6% and 4.1%, respectively between 2011 and 2030. This represents incremental airline fleet growth of 40,000 aircraft over the next 20 years, with between 16,000 and 20,000 additions to the leased fleet. Growth of passenger air travel in emerging countries and regions plus the growth of low-cost carriers globally are important drivers of aviation growth and represent key growth opportunities for aircraft lessors.

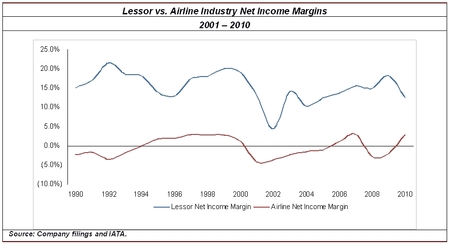

Aircraft operating leases are multi-year in nature, typically 6 to 10 years for new aircraft, depending upon the age of the aircraft. Due to the long-term duration of lease contracts, aircraft lessor revenues and earnings tend to be more stable than for their airline lessee customers. Aircraft lessors are also less directly susceptible to the variations in passenger demand, fares, fuel, labour costs and other expenses that historically have caused much of the volatility in airline industry profitability. Aircraft lessors are exposed to the credit quality of their customers, however, which is directly affected by these issues, and use contractual terms in their leases, including security deposits, maintenance reserves, return conditions, payment of rent in advance and other mechanisms to protect revenue and the value of their portfolio. Despite volatility in the commercial aviation sector over the last 20 years, aircraft leasing companies have experienced relatively low and manageable volatility in their profitability and returns. While airlines experience dramatic swings in net profit through the cycle, aircraft lessors are steadier and less susceptible to the extremes of the industry cycle. During three major cyclical declines in the aviation business - in 1991, 2001 and 2009 - lessors demonstrated their ability to maintain profitability, in contrast to the airline sector, as demonstrated above. Aircraft have the ability to generate strong equity returns for investors over a long-term investment horizon. Investing in aircraft leasing equity is inherently long-term in nature due to the extended useful life and lease terms associated with aircraft. Commercial jet aircraft have economic lives of 25 years or more, during which they generate cash flow for their lessor owners from multi-year lease contracts. Typically an aircraft can be leased 4 to 6 times over its 25 year life on leases with contract terms of typically 6 to 10 years, depending upon the age of the aircraft. During an aircraft’s useful life, maximizing lease income and an aircraft’s residual value is critical to generating strong returns. Acquiring aircraft with a proven ability to retain residual value allows an aircraft lessor to continue to generate robust lease income over many cycles, leases and years while minimizing risk of loss on a future sale of the aircraft.

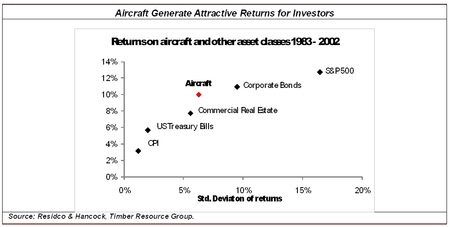

Aircraft have consistently generated stable risk-adjusted returns for investors throughout the economic cycles, outperforming many other asset classes in terms of returns and volatility. Structuring a well-managed portfolio of aircraft diversified across different lessees, geographies, aircraft types and lease expirations can generate steady long-term risk-adjusted equity returns across multiple industry cycles. Investing across these cycles requires active portfolio management as the cycles influence not only aircraft values, but also the relationship between supply (seats and aircraft) and demand (passengers), airline profitability, financial liquidity and aircraft trading activity, all of which influence the ability to generate returns from aircraft investments. Aircraft are a critical element of the global transportation infrastructure. As global economic growth continues to generate strong demand for passenger air travel and, in turn, a growing global fleet, demand for aircraft leasing equity and the associated generation of strong equity returns is also expected to grow steadily as an investment class. Dick Forsberg is head of risk and strategy at Avolon. This article was published on September 15th 2011 |