- Latest Edition (April 18th): Lessor says "best first quarter since 2020"

- April 4th edition: Capital markets back aircraft leasing

- March 21st edition: Leasing companies report record results; look ahead with confidence

- March 7th edition: Good conditions will "persist for many years" - Kelly

- February 22nd edition: Big widebody orders in Singapore

- February 8th edition: Bright opportunities pull in new investors

|

Redeliveries still source of tension between lessor and lessee

Trends in redeliveries over the past two years suggest there have been some improvements in the understanding between lessors and lessees of the challenges involved in the process. But a recent survey by independent aviation consultancy IBA also identified increasing returns, combined with a lack of lessees, as an indicator of increasing concern about liquidity and as being a factor in the slight, but noticeable, increase in disputes when lessors receive unplaced aircraft.

While understanding of the effort involved in redeliveries has improved, execution still appears to be a real challenge for both lessees and lessors, with engine costs being a key driver in an increase in overspends since 2016.

In preparing an up-to-date picture of the redelivery landscape, independent aviation consultancy IBA surveyed lessors and lessess. In its 2016 report IBA received 72 responses, split approximately two thirds/one third between lessors and lessees. The latest survey had 140 responses, split close to evenly between the two categories.

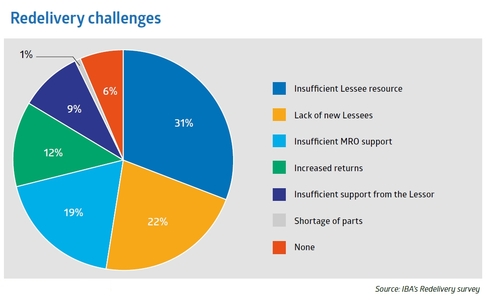

In the latest survey IBA found that insufficient lessee resource, increased returns, scarce support from the lessor and insufficient MRO support were cited as being causes for over half of the redelivery challenges identified by respondents. The proportion of lessors who feel that lessees engage too late in the redelivery process increased from 47 per cent in its 2016 survey to almost 60 per cent. On a positive note, one of the largest swings in results between the two surveys was a significant decline in ‘underestimation of effort’ being given as a primary reason for redelivery overspends. The authors add that this is 'an encouraging trend given the plethora of new entrants.' In respect of potential current year difficulties, MROs were flagged as a bottleneck by one in five respondents, although the MROs also complain they are engaged too late by the lessees. Several MROs interviewed by IBA in conjunction with the survey said they found the returning lessees to be reasonably organised for the End of Lease check (EOL). But they were more frustrated when dealing with returning lessors seeking last minute changes to meet the next lessee’s demands. Lack of lessees – especially for widebodies – was also identified as a concern. 'We are seeing the return of used widebodies after the first lease, regardless of the extension offer,' IBA said. The consultants also say that although extensions have been the order of the day for the last two years, 'increasing returns combined with a lack of lessees would indicate increasing concern for liquidity and would also feed the slight, but noticeable, increase in disputes which can occur when a lessor receives an unplaced aircraft.' The latest survey found a switch in lessee attitudes, moving from a majority perception that they engage early enough, to almost mirroring that of the lessors that lessees engage too late. Based on this, the authors say, their conclusions can be defined into tactical and strategic proposals. 'Tactically, there are further improvements to be made in planning and resourcing redeliveries ... MRO support accounted for over half of our responses on 2018 redelivery challenges. Combine that with late engagement, the most frequently flagged reason for late redeliveries, and you have a perfect recipe for a likely overspend. 'Strategically, there are potential red flags emerging around supply. Twenty two per cent of respondents flagged a lack of new lessees as a concern, a sentiment also voiced when asking for additional comments, where more concerns were flagged around liquidity than previously.' The authors add, however, the current picture does not yet suggest that more popular aircraft are failing to be re-leased. As of early May 2018, IBA's own research identified that the number of passenger widebody returns had reached 48, with two thirds re-leasing within just a few months. 'It is unknown as to whether the remaining 17 have homes to go to just yet but their average age is 17 years old, whilst the fast movers averaged at just 10 years,' the consultants say. 'Unsurprisingly, half of those that remain parked are four-engined aircraft, whilst the remaining half are made up of more challenging 777 classics and A330-200s. Encouragingly, those that have been re-leased include a good number of older 767-300ERs, a large number of A330-200s and 300s with even the odd 777-300ER and A340-600 for good measure.'

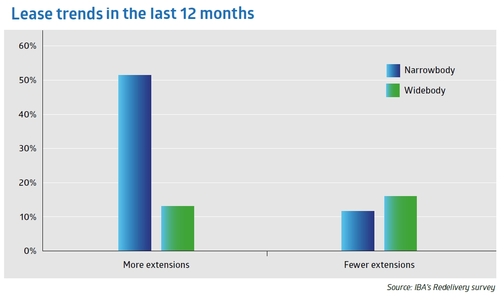

On the question of the primary reason for a late redelivery, IBA says there are fewer disagreements over contracts, echoing the improvements in drafting it has seen in the last two years. 'However, while ambiguous terms have reduced, there has been an increase in lessees' demands being met. For example, delivery conditions for interior configuration being a lessor’s obligation. For redeliveries the top tier lessees are able to negotiate diluted conditions, much less than half life in some cases.' But on a less positive note, it says engagement is still taking place too late and it recommends that engaging around the options should commence at least 15 months out. IBA also says that as more operators have either built up their own redelivery resource or outsourced to dedicated resources, it was surprised that the feedback around the lessees' technical teams being focused on keeping the fleet flying, not redelivering, had crept up a little. Anecdotally, the authors add, the airline collapses of 2017 also caused a spike in demand for delivery and redelivery resource. 'Also there are big differences in what resource is actually available at the airline. Clearly the LCCs redelivering aircraft have much less manpower in-house than a legacy carrier. We anticipate further issues in this area, especially since some LCCs appear to be pushing the obligation onto their MRO and that, in itself, causes conflict on points such as records/certification.' Asked which area of the aircraft is most challenging to redeliver on time and on budget, respondents still identify records as a primary challenge. 'The concept of lessors hiring cheap labour to scan records at the last minute is compelling but risky and while systems and digitisation are certainly improving, translations and back-to-birth traceability remain a perennial concern,' the report's authors says. They expressed surprise, however, that interiors and interior items did not generate more responses, as in the company's own direct experience interior condition has proved a point of robust negotiation. Asked what changes to end of lease trends they had noticed in the last 12 months, a significant proportion of respondents identified an increase in extensions, driven by such factors as delays of A320neo/737MAX deliveries as a result of EIS engine issues; continued relatively low fuel price; regional instability impacting demand and fuel price; continued demand for capacity; the fact that traffic growth remains robust and an extension can be achieved at a reasonable rate, especially on widebodies. Against this, fewer extensions were identified as a worry for lessors as the options to find new homes is tough, despite deals being offered (eg lower rents), and some regional distress in respect of Qatar/Middle East and US competition. |

Vol. 8 Issue 11 of Aviation Finance